Page 168 - CalcBus_Flipbook

P. 168

20-12 Profitability & Performance Measures CH 20]

Inventory Turnover Ratio: An efficiency ratio that measures how effectively

inventory is managed by comparing cost of goods sold with average inventory for a period.

This calculation indicates how many times average inventory is sold (turned over) during a

reporting period. The equation for this ratio is:

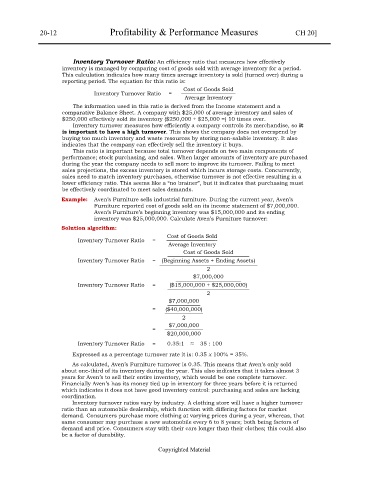

Cost of Goods Sold

Inventory Turnover Ratio = ——————————

Average Inventory

The information used in this ratio is derived from the Income statement and a

comparative Balance Sheet. A company with $25,000 of average inventory and sales of

$250,000 effectively sold its inventory ($250,000 ÷ $25,000 =) 10 times over.

Inventory turnover measures how efficiently a company controls its merchandise, so it

is important to have a high turnover. This shows the company does not overspend by

buying too much inventory and waste resources by storing non-salable inventory. It also

indicates that the company can effectively sell the inventory it buys.

This ratio is important because total turnover depends on two main components of

performance; stock purchasing, and sales. When larger amounts of inventory are purchased

during the year the company needs to sell more to improve its turnover. Failing to meet

sales projections, the excess inventory is stored which incurs storage costs. Concurrently,

sales need to match inventory purchases, otherwise turnover is not effective resulting in a

lower efficiency ratio. This seems like a “no brainer”, but it indicates that purchasing must

be effectively coordinated to meet sales demands.

Example: Aven’s Furniture sells industrial furniture. During the current year, Aven’s

Furniture reported cost of goods sold on its income statement of $7,000,000.

Aven’s Furniture’s beginning inventory was $15,000,000 and its ending

inventory was $25,000,000. Calculate Aven’s Furniture turnover:

Solution algorithm:

Cost of Goods Sold

Inventory Turnover Ratio = —————————-

Average Inventory

Cost of Goods Sold

———————————————

Inventory Turnover Ratio = (Beginning Assets + Ending Assets)

——————————————————

2

$7,000,000

————————————

Inventory Turnover Ratio = ($15,000,000 + $25,000,000)

———————————————

2

$7,000,000

——————

= ($40,000,000)

———————

2

$7,000,000

= ———————

$20,000,000

Inventory Turnover Ratio = 0.35:1 ≈ 35 : 100

Expressed as a percentage turnover rate it is: 0.35 x 100% = 35%.

As calculated, Aven’s Furniture turnover is 0.35. This means that Aven’s only sold

about one-third of its inventory during the year. This also indicates that it takes almost 3

years for Aven’s to sell their entire inventory, which would be one complete turnover.

Financially Aven’s has its money tied up in inventory for three years before it is returned

which indicates it does not have good inventory control: purchasing and sales are lacking

coordination.

Inventory turnover ratios vary by industry. A clothing store will have a higher turnover

ratio than an automobile dealership, which function with differing factors for market

demand. Consumers purchase more clothing at varying prices during a year, whereas, that

same consumer may purchase a new automobile every 6 to 8 years; both being factors of

demand and price. Consumers stay with their cars longer than their clothes; this could also

be a factor of durability.

Copyrighted Material