Page 22 - Bus101FlipBook

P. 22

1-10 Business and Economic Environments [CH 1

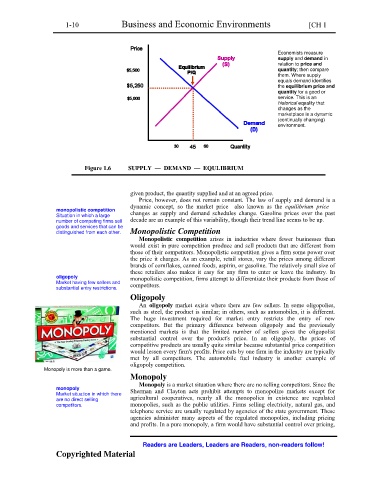

Economists measure

supply and demand in

relation to price and

quantity; then compare

them. Where supply

equals demand identifies

the equilibrium price and

quantity for a good or

service. This is an

historical equality that

changes as the

marketplace is a dynamic

(continually changing)

environment.

Figure 1.6 SUPPLY — DEMAND — EQULIBRIUM

given product, the quantity supplied and at an agreed price.

Price, however, does not remain constant. The law of supply and demand is a

dynamic concept, so the market price—also known as the equilibrium price—

monopolistic competition changes as supply and demand schedules change. Gasoline prices over the past

Situation in which a large

number of competing firms sell decade are an example of this variability, though their trend line seems to be up.

goods and services that can be

distinguished from each other. Monopolistic Competition

Monopolistic competition arises in industries where fewer businesses than

would exist in pure competition produce and sell products that are different from

those of their competitors. Monopolistic competition gives a firm some power over

the price it charges. As an example, retail stores, vary the prices among different

brands of cornflakes, canned foods, aspirin, or gasoline. The relatively small size of

these retailers also makes it easy for any firm to enter or leave the industry. In

oligopoly monopolistic competition, firms attempt to differentiate their products from those of

Market having few sellers and competitors.

substantial entry restrictions.

Oligopoly

An oligopoly market exists where there are few sellers. In some oligopolies,

such as steel, the product is similar; in others, such as automobiles, it is different.

The huge investment required for market entry restricts the entry of new

competitors. But the primary difference between oligopoly and the previously

mentioned markets is that the limited number of sellers gives the oligopolist

substantial control over the product's price. In an oligopoly, the prices of

competitive products are usually quite similar because substantial price competition

would lessen every firm's profits. Price cuts by one firm in the industry are typically

met by all competitors. The automobile fuel industry is another example of

oligopoly competition.

Monopoly is more than a game.

Monopoly

Monopoly is a market situation where there are no selling competitors. Since the

monopoly Sherman and Clayton acts prohibit attempts to monopolize markets except for

Market situation in which there

are no direct selling agricultural cooperatives, nearly all the monopolies in existence are regulated

competitors. monopolies, such as the public utilities. Firms selling electricity, natural gas, and

telephone service are usually regulated by agencies of the state government. These

agencies administer many aspects of the regulated monopolies, including pricing

and profits. In a pure monopoly, a firm would have substantial control over pricing,

Readers are Leaders, Leaders are Readers, non-readers follow!

Copyrighted Material