Page 56 - Account for Ag - 2019

P. 56

9-20 Accounting for Agriculture CH 9]

Name:

QUESTIONS

1. (a) What is the commercial practice regarding the denominator of the fraction for time in interest calculation?

(b) Give the basic formula for computing interest.

(a) _____________________________________________________________________________

________________________________________________________________________________

________________________________________________________________________________

(b) ______________________________________________________________________________

________________________________________________________________________________

2. Explain the meaning of the following terms:

(a) Discounting a note.

(b) Discount

(c) Proceeds.

(d) Discount rate.

(a) Discounting a note: _____________________________________________________________

________________________________________________________________________________

________________________________________________________________________________

(b) Discount: ____________________________________________________________________

(c) Proceeds. _____________________________________________________________________

(d) Discount rate __________________________________________________________________

________________________________________________________________________________

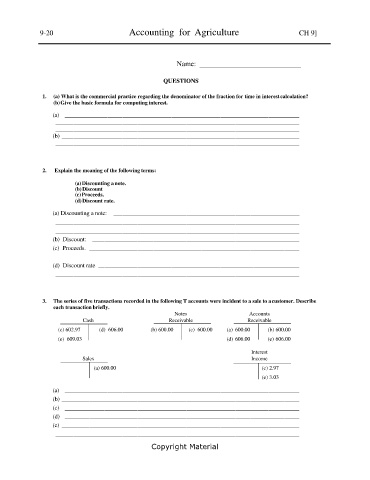

3. The series of five transactions recorded in the following T accounts were incident to a sale to a customer. Describe

each transaction briefly.

Notes Accounts

Cash Receivable Receivable

(c) 602.97 (d) 606.00 (b) 600.00 (c) 600.00 (a) 600.00 (b) 600.00

(e) 609.03 (d) 606.00 (e) 606.00

Interest

Sales Income

(a) 600.00 (c) 2.97

(e) 3.03

(a) _____________________________________________________________________________

(b) ______________________________________________________________________________

(c) _____________________________________________________________________________

(d) _____________________________________________________________________________

(e) ______________________________________________________________________________

________________________________________________________________________________

Copyright Material