Page 83 - CalcBus_Flipbook

P. 83

CH 10] Calculating Business 10-5

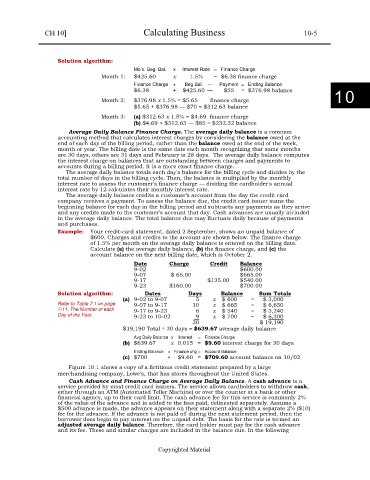

Solution algorithm:

Mo’s. Beg. Bal. x Interest Rate = Finance Charge

Month 1: $425.60 x 1.5% = $6.38 finance charge

Finance Charge + Beg Bal. — Payment = Ending Balance

$6.38 + $425.60 — $55 = $376.98 balance

Month 2: $376.98 x 1.5% = $5.65 finance charge 10

$5.65 + $376.98 — $70 = $312.63 balance

Month 3: (a) $312.63 x 1.5% = $4.69 finance charge

(b) $4.69 + $312.63 — $85 = $232.32 balance

Average Daily Balance Finance Charge. The average daily balance is a common

accounting method that calculates interest charges by considering the balance owed at the

end of each day of the billing period, rather than the balance owed at the end of the week,

month or year. The billing date is the same date each month recognizing that some months

are 30 days, others are 31 days and February is 28 days. The average daily balance computes

the interest charge on balances that are outstanding between charges and payments to

accounts during a billing period. It is a more exact finance charge.

The average daily balance totals each day's balance for the billing cycle and divides by the

total number of days in the billing cycle. Then, the balance is multiplied by the monthly

interest rate to assess the customer's finance charge — dividing the cardholder's annual

interest rate by 12 calculates their monthly interest rate.

The average daily balance credits a customer’s account from the day the credit card

company receives a payment. To assess the balance due, the credit card issuer sums the

beginning balance for each day in the billing period and subtracts any payments as they arrive

and any credits made to the customer’s account that day. Cash advances are usually included

in the average daily balance. The total balance due may fluctuate daily because of payments

and purchases.

Example: Your credit-card statement, dated 2 September, shows an unpaid balance of

$600. Charges and credits to the account are shown below. The finance charge

of 1.5% per month on the average daily balance is entered on the billing date.

Calculate (a) the average daily balance, (b) the finance charge, and (c) the

account balance on the next billing date, which is October 2.

Date Charge Credit Balance

9-02 $600.00

9-07 $ 65.00 $665.00

9-17 $125.00 $540.00

9-23 $160.00 $700.00

Solution algorithm: Dates Days Balance Sum Totals

(a) 9-02 to 9-07 5 x $ 600 = $ 3,000

Refer to Table 7.1 on page 9-07 to 9-17 10 x $ 665 = $ 6,650

7-11, The Number of each 9-17 to 9-23 6 x $ 540 = $ 3,240

Day of the Year. 9-23 to 10-02 9 x $ 700 = $ 6,300

30 $ 19,190

$19,190 Total ÷ 30 days = $639.67 average daily balance

Avg Daily Balance x Interest = Finance Charge

(b) $639.67 x 0.015 = $9.60 interest charge for 30 days

Ending Balance + Finance chg = Account Balance

(c) $700 + $9.60 = $709.60 account balance on 10/02

Figure 10.1 shows a copy of a fictitious credit statement prepared by a large

merchandising company, Lowe’s, that has stores throughout the United States.

Cash Advance and Finance Charge on Average Daily Balance. A cash advance is a

service provided by most credit card issuers. The service allows cardholders to withdraw cash,

either through an ATM (Automated Teller Machine) or over the counter at a bank or other

financial agency, up to their card limit. The cash advance fee for this service is commonly 2%

of the value of the advance and is added to the fees paid, delineated separately. Assume a

$500 advance is made, the advance appears on their statement along with a separate 2% ($10)

fee for the advance. If the advance is not paid off during the next statement period, then the

borrower does begin to pay interest on the unpaid debt. The basis for the rate is termed an

adjusted average daily balance. Therefore, the card holder must pay for the cash advance

and its fee. These and similar charges are included in the balance due. In the following

Copyrighted Material